Beyond Guesswork: The 4-Step Formula to Determine the “Value” of Your Life

Use this dead-simple DIME formula to calculate your ideal coverage and protect your loved ones without breaking the bank.

Insurance salesmen won't tell you this, but you may not need 10 million dollars of life insurance.

Because these commission-hungry agents often push policies that far exceed your actual needs, leaving you overinsured and overpaying.

It’s a weird thing to think our life has a “value” attached to it, right? Of course - it feels weird to talk about, but the reality is it's true. Your life has tremendous value to your loved ones.

Luckily, determining the right amount of life insurance coverage is simple if you know where to start.

And unlike those pushy salesmen, this won't cost you thousands in unnecessary premiums.

Instead, use this dead-simple DIME formula to calculate your ideal coverage and protect your loved ones without breaking the bank.

How to Use the DIME Formula to Get the Right Life Insurance Coverage

The DIME formula helps you break down your financial obligations into four key areas.

Step 1: Calculate your Debt and final expenses.

The biggest thing I tell people when it comes to this topic is this; don’t leave your debts for someone else to handle. “A man ensures he has his affairs in order” - Tommy Shelby, for my Peaky Blinders fans out there.

Add up all outstanding debts, including car loans, and credit card balances. Don't forget to include an estimate for funeral costs and other end-of-life expenses.

Tip: Round up slightly to account for any unexpected debts or costs. (Life isn’t getting any cheaper)

Step 2: Determine your Income replacement needs.

Multiply your annual income by the number of years your family would need support. A common mistake is overestimating this timeframe. Oftentimes you’ll hear salesmen claim people need 20x income replacement. In some instances, this may be the case - but every situation is different. Maybe 5-10 years is enough. All depends on how long you want to ensure everyone is taken care of.

Step 3: Account for your Mortgage payoff.

This ensures your family can stay in their home without financial strain.

The absolute last thing you want your family to have to worry about is losing the home on top of the fact that they just lost you. Ensuring that this is handled provides significant relief to your family knowing there is a major expense they no longer have to stress about on a monthly basis.

Step 4: Estimate Education costs for your children.

Consider future tuition, room and board, books, and other education-related expenses for each child. Research the current costs of colleges your children might attend and factor in potential inflation.

Unlike some of the other parts of the DIME formula, this is one that isn’t what I’d call imperative. If you’d like to plan for education costs, absolutely include it - but it’s not as much of a requirement as debt payoff & income replacement in my opinion.

Tip: Use education savings calculators available online to get a more accurate estimate.

By following these steps, you'll have a clear picture of your family's financial needs in your absence, ensuring they're protected.

If you have some coverage through work, that's great - but likely isn’t enough and doesn’t follow you if you leave that job. Having personal coverage often ensures you are always covered & have a sufficient amount for your needs.

Let's look at a real-world example

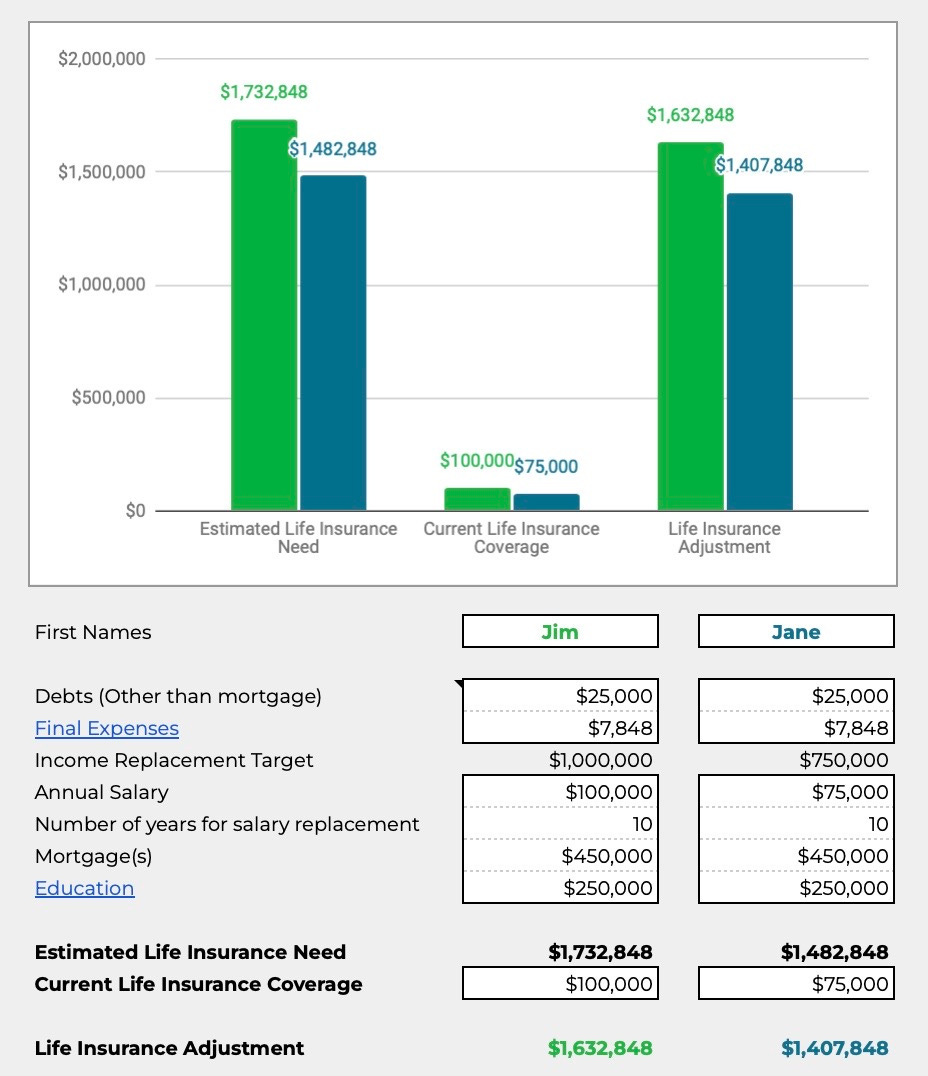

Jim & Jane are married at age 32 with three children.

They bring home $175,000 as a household ($100k & $75k respectively)

Have a $450,000 mortgage

$25,000 in small debts (Credit Card & Car Loans)

One of their big goals is to send all three children to Penn State University, and they estimate this will cost them roughly $250k by the time all three are through.

Would like to have 10 years of income covered if something happened to them

Our handy chart from our Private Client Workbook (there are online calculators as well) tells us that this couple likely has a need of ~$1.7 & ~$1.5 million dollars in total coverage.

Because they have a small policy through work (1x Salary) we deduct that from the estimated life insurance need & that gives us the recommended life insurance adjustment.

For a healthy 32 year old male, $1.6 million in coverage for a 30 year term policy would cost $1,099/year - or roughly $91.62/month. A female with the same situation would cost roughly $870/ year or $72.47 a month. (Women are generally healthier and live longer than men & are hence cheaper to insure)

This is a no brainer when it comes to protecting your family. We won't get into types of life insurance as there are obviously different kinds & they have different costs associated (topic for another day). But for most young individuals looking for maximum protection for the cheapest cost - term is the way to go.

Last point - let's say you see those prices and think that's a bit too high for the budget right now. No problem at all, you can always pull back knowing we just won't have EVERYTHING we wanted covered - which is fine. As we noted before, we can always make adjustments as life evolves.

Now, let's explore why this formula works so well.

Why the DIME Formula Gives You the Right Coverage

The DIME formula is effective because it's based on real financial needs, not guesswork.

It's personalized to your situation. By calculating your specific debts, income, mortgage, and education costs, you're getting a tailored assessment. This precision ensures you're neither under-insured nor over-insured, giving you peace of mind and financial efficiency.

It's flexible and can be adjusted over time. As your life circumstances change – paying off debts, children growing up, or career advancements – you can easily recalculate your needs. This adaptability means your coverage always aligns with your current life stage, preventing you from paying for unnecessary coverage.

It provides a clear rationale for your coverage amount. When you understand the components of your life insurance need, you're better equipped to resist upselling tactics. This knowledge empowers you to make confident decisions about your coverage, ensuring you get what you need without succumbing to fear-based sales pitches.

Common Misconceptions About Life Insurance

Before we conclude, let's address some common misconceptions:

"I'm young and healthy, so I don't need life insurance." - Unexpected events can happen at any age, and insurance is often cheaper when you're young and healthy.

"My employer-provided insurance is enough." - As mentioned earlier, this coverage is often insufficient and doesn't follow you if you change jobs.

"Life insurance is too expensive." - Term life insurance can be surprisingly affordable, especially when balanced against the financial security it provides.

The True Value of Your Life Goes Beyond Numbers

Remember, while the DIME formula helps quantify your financial obligations, the true value of your life is immeasurable. This calculation is simply a tool to ensure your loved ones' financial stability, allowing them to focus on your legacy rather than financial worries.

Conclusion

The DIME formula offers a practical, personalized approach to calculating your life insurance needs. By considering your Debts, Income, Mortgage, and Education expenses, you can arrive at a coverage amount that truly reflects your family's financial requirements. Remember, the goal isn't to leave behind a fortune, but to ensure your loved ones can maintain their quality of life and pursue their dreams even in your absence.

Don't let pushy salesmen or generic rules of thumb dictate your coverage. Take control of your financial future by using this simple yet powerful tool. Reassess your needs periodically as your life circumstances change, and adjust your coverage accordingly. In doing so, you'll find the peace of mind that comes from knowing you've taken a thoughtful, measured approach to protecting what matters most - your family's financial security and your lasting legacy.

Take Action

Now that you understand the DIME formula, take the first step towards securing your family's future. Grab a pen and paper, or open a spreadsheet, and start calculating your DIME components. Remember, this is a starting point - for complex situations or if you're unsure, consider consulting with a financial professional who can provide personalized advice based on your unique circumstances.

See you next week,

Whenever you're ready, there are 2 other ways we can help you:

Opulus Method Digital Course: Join 350+ students inside the Opulus Method. In just 90 minutes, learn a proven system to secure your financial freedom without sacrificing your lifestyle.

Join Opulus as a Client: We'll join forces to create a personal financial plan and investment strategy to secure your financial future. Let us handle the complex details. Go ahead and enjoy your life.

Opulus, LLC (“Opulus”) is a registered investment advisor in Pennsylvania and other jurisdictions where exempted. Registration as an investment advisor does not imply any specific level of skill or training.

The content of this newsletter is for informational purposes only and does not constitute financial, tax, legal, or accounting advice. It is not an offer or solicitation to buy or sell any securities or investments, nor does it endorse any specific company, security, or investment strategy. Readers should not rely on this content as the sole basis for any investment or financial decisions.

Past performance is not indicative of future results. Investing involves risks, including the potential loss of principal. There is no guarantee that any investment strategies discussed will result in profits or avoid losses.

All information is provided "as-is" without any warranties, express or implied. Opulus does not warrant the accuracy, completeness, or reliability of the information presented. Opinions expressed are those of the authors, Ryan Greiser and Francis Walsh, and are subject to change without notice.

Opulus is not responsible for any errors or omissions, nor for any direct, indirect, or consequential damages resulting from the use or reliance on this information. Use of the content is at your own risk. This content is not intended as an offer or solicitation in any jurisdiction where such an offer or solicitation would be illegal.