W-2 Millennials: 11 Tax Optimization Strategies You Can't Afford to Miss

Do you feel like taxes are taking a bigger bite out of your paycheck than they should? With the right tax strategies, you can keep more of your money and grow your wealth.

As a millennial navigating the complexities of work, savings, and future planning, it can feel like taxes are constantly eating into your paycheck.

But it doesn’t have to be this way. There are key tax strategies that W2 employees like you can use to minimize taxes and increase your financial stability.

Today, we’ll break down 11 essential tax optimization tactics that can help you save now and in the long run.

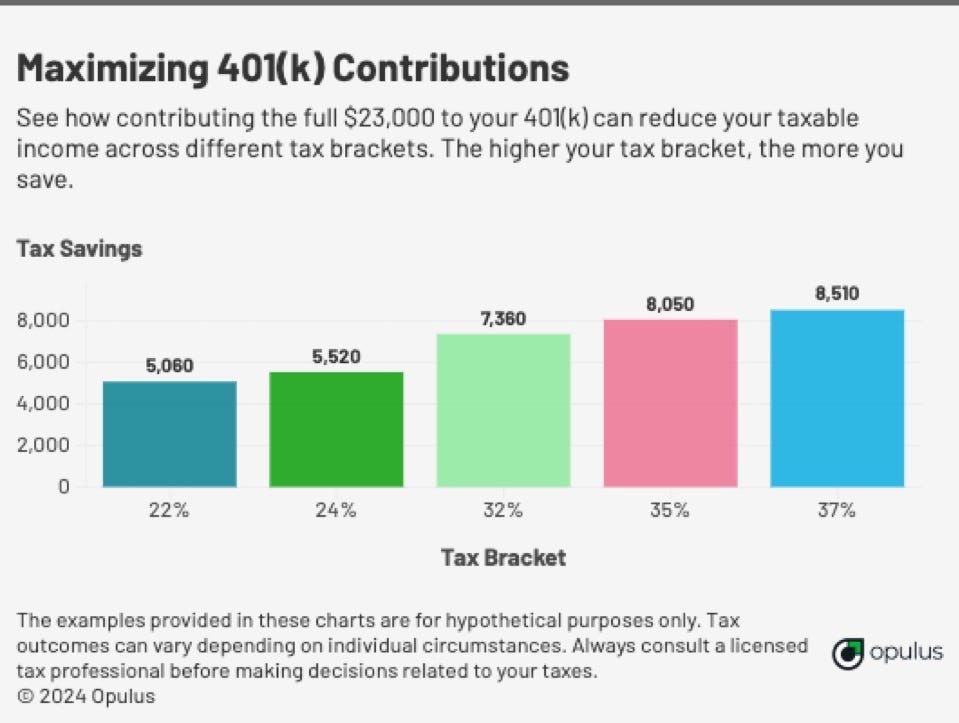

1 - Max Out Your 401k Contributions

If you want to save on taxes while building your retirement, your 401k should be your first stop. Max out the $23,000 contribution limit (for 2024), and grab the employer match. The best money is free money. Consistency here is key.

Be aware of: Track your total contributions if you switch jobs or have multiple 401k plans in a year. The IRS limits apply to your total contributions across all plans, and exceeding them can lead to penalties.

2 - Leverage Your HSA for Tax Savings

The HSA is a triple win: upfront tax deductions, tax-free growth, and tax-free withdrawals for qualified medical expenses. If you're on a high-deductible health plan, contribute the maximum allowed: $4,150 for individuals or $8,300 for families in 2024. This is one of the most tax-advantaged accounts out there, and it can even be used as a supplemental retirement account if you're healthy.

Be aware of: Stick to the IRS's strict guidelines for eligible medical expenses. Non-qualified withdrawals before age 65 incur penalties, so save receipts for qualified expenses just in case.

See below for 2023 numbers:

3 - Use the Backdoor to Fund a Roth IRA

You may earn too much to contribute directly to a Roth IRA, but you can still benefit from tax-free growth through the backdoor Roth strategy. Here’s how: First, roll any pre-tax IRA funds into your 401k if your plan allows, which clears the way for tax-efficient conversions. Then contribute to a traditional IRA and convert it to a Roth. This strategy allows both you and your spouse to bypass income limits.

Be aware of the pro-rata rule. If you have other traditional IRAs with pre-tax funds, your conversion will be partially taxable, so consider rolling those funds into your 401k first to avoid complications.

4 - Take Advantage of Lower Capital Gains Tax Rates

When it comes to investments, long-term gains are taxed more favorably than short-term gains. Holding investments for more than a year qualifies you for long-term capital gains tax rates of 0%, 15%, or 20%, depending on your income level. The longer you hold, the better the compounding, and the lower the tax hit.

Be aware of: Timing is crucial. If you sell before holding for a full year, your gains will be taxed at your ordinary income tax rate, which can be significantly higher.

5 - Offset Gains with Tax-Loss Harvesting

Facing capital gains taxes? Use tax-loss harvesting to your advantage by selling losing investments to offset gains. For example, if you made $5,000 in gains but sell investments at a $3,000 loss, you'll only pay taxes on the net $2,000. This smart end-of-year strategy can reduce your tax bill while keeping your money working for you.

Be aware of the wash-sale rule. If you buy the same or a "substantially identical" investment within 30 days of selling at a loss, you won’t be able to claim the loss. Make sure you plan your trades carefully.

6 - Start a 529 Plan for Future Education

Even if you don’t have kids yet, opening a 529 plan early allows you to benefit from tax-free investment growth over time. Some states even offer tax breaks for contributions. And if your future children don’t need the funds, you can always change the beneficiary to another family member or even use it yourself for qualifying educational expenses.

Be aware of state-specific rules. Not all states offer tax benefits for 529 contributions, so check your state’s regulations to maximize your benefits. You can also invest in out-of-state 529 plans, which might offer better incentives.

7 - Make Your Investments More Tax-Efficient

To minimize taxes, keep tax-inefficient investments like real estate investment trusts (REITs) or bond funds inside tax-advantaged accounts like IRAs or 401ks. On the other hand, place tax-efficient investments like index funds in taxable accounts. Municipal bonds are also a great option for those in high-tax states, as they offer tax-free interest at the federal level—and sometimes at the state level too.

Be aware of the tax treatment of specific investments. While municipal bonds are generally tax-free at the federal level, some may still be taxable at the state level, so research before you invest.

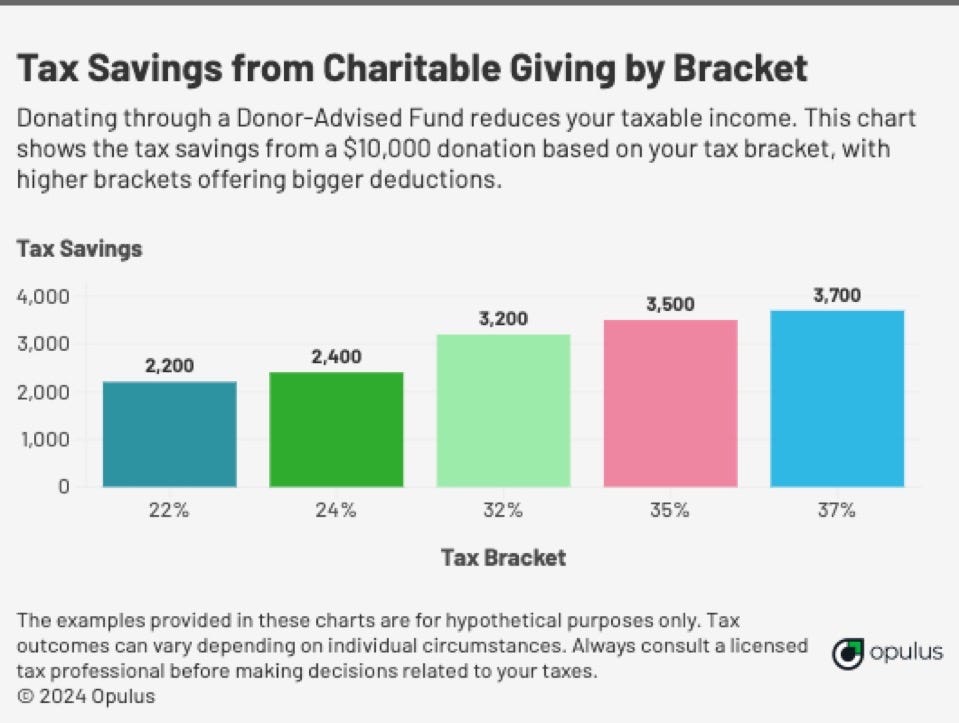

8 - Donate Appreciated Assets for a Tax Break

If you have investments that have significantly appreciated, donating them directly to charity can offer dual benefits: you’ll avoid capital gains taxes on the appreciation, and you’ll get a tax deduction for the asset. A Donor-Advised Fund (DAF) is a flexible way to manage charitable donations over time while getting the immediate tax benefit.

Be aware of Charitable deduction limits. For most taxpayers, charitable deductions are capped at 60% of your adjusted gross income (AGI), though you can carry forward excess contributions for up to five years.

9 - Consider Direct Indexing for More Control

Direct indexing allows you to own individual stocks instead of a broad-market ETF, giving you more control over tax-loss harvesting and capital gains management. This strategy is particularly useful for high-net-worth investors who want to customize their portfolios and optimize for taxes.

Be aware of the added complexity and cost. Direct indexing may come with higher transaction fees and requires more active management compared to low-cost index funds or ETFs, so consider whether the benefits justify the extra effort.

10 - Tax Savings on Childcare with a Dependent Care FSA

A Dependent Care Flexible Spending Account (FSA) allows you to set aside up to $5,000 in pre-tax dollars to cover eligible childcare expenses, such as daycare, preschool, or summer camps. By contributing to a Dependent Care FSA, you reduce your taxable income, which can lead to significant tax savings while covering the cost of necessary care for your children.

Be aware of: You must use the funds during the plan year, or they’ll be forfeited (though some plans offer a grace period). Also, the IRS has strict guidelines on what qualifies as eligible expenses, so make sure your childcare provider meets the criteria.

11 - Energy-Efficient Home Upgrades for Big Tax Credits

If you’re a homeowner, energy-efficient improvements can offer significant tax savings while lowering your utility bills long-term. Here’s how you can take advantage of the tax credits:

Install solar, wind, or geothermal systems and claim 30% of the cost back through the Residential Clean Energy Credit. There’s no upper limit on the credit, making this a huge win for anyone looking to go green.

Upgrade windows, doors, insulation, or other energy-efficient improvements and get up to $3,200 in tax credits. It’s a win-win for your wallet and the planet, with lower energy bills and bigger tax breaks.

Install energy-efficient heat pumps or water heaters to claim up to $2,000 in additional tax credits, further cutting down your energy costs over time.

By combining these strategies, you can not only enjoy substantial tax savings but also make your home more energy-efficient and environmentally friendly.

Be aware of the timing and eligibility requirements for these credits. Some improvements may need to meet specific energy-efficiency standards to qualify, and the credits may only apply to your primary residence. Make sure to consult IRS guidelines or a tax professional before making major upgrades.

Conclusion:

By applying these tax-saving strategies, you can keep more of your hard-earned money and grow your wealth for the future.

Whether you’re maximizing your retirement contributions, making your investments more tax-efficient, or leveraging the flexibility of a side hustle, smart tax planning can significantly impact your financial journey.

Take action now, and you’ll be in a stronger position when tax season rolls around.

Thanks for reading. We'll see you next week.

Whenever you're ready, there are 2 other ways we can help you:

Opulus Method Digital Course: Join 350+ students inside the Opulus Method. In just 90 minutes, learn a proven system to secure your financial freedom without sacrificing your lifestyle.

Join Opulus as a Client: We'll build your personalized strategy to reduce taxes, boost your income, and grow your wealth. Live life on your terms—we'll execute the financial strategy to get you there.

Opulus, LLC (“Opulus”) is a registered investment advisor in Pennsylvania and other jurisdictions where exempted. Registration as an investment advisor does not imply any specific level of skill or training.

The content of this newsletter is for informational purposes only and does not constitute financial, tax, legal, or accounting advice. It is not an offer or solicitation to buy or sell any securities or investments, nor does it endorse any specific company, security, or investment strategy. Readers should not rely on this content as the sole basis for any investment or financial decisions.

Past performance is not indicative of future results. Investing involves risks, including the potential loss of principal. There is no guarantee that any investment strategies discussed will result in profits or avoid losses.

All information is provided "as-is" without any warranties, express or implied. Opulus does not warrant the accuracy, completeness, or reliability of the information presented. Opinions expressed are those of the authors, Ryan Greiser and Francis Walsh, and are subject to change without notice.

Opulus is not responsible for any errors or omissions, nor for any direct, indirect, or consequential damages resulting from the use or reliance on this information. Use of the content is at your own risk. This content is not intended as an offer or solicitation in any jurisdiction where such an offer or solicitation would be illegal.