3 Compelling Reasons to Keep Your Mortgage (and 3 to Pay It Off Early)

Leverage your biggest debt into your strongest asset.

"Pay off your mortgage or invest?"

51% of Americans say, "Pay it off," but the math often tells a different story.

This decision could make or break your wealth-building strategy. And let me tell you, it's not as straightforward as most "experts" claim.

I've helped hundreds of clients navigate this exact crossroads.

Why does it come up so often?

Because it's where financial logic meets real-life emotions in personal finance.

Here's what we're diving into:

3 compelling reasons to keep your mortgage

3 powerful arguments for paying it off early

A hybrid approach that might give you the best of both worlds

By the end, you'll have a framework to make the best decision for your financial future. One that aligns with both your wealth goals and your peace of mind.

Let's get into it.

Reasons to Keep Your Mortgage

1. Opportunity Cost

Here's the truth: Your cash might work harder elsewhere.

Think about it. Historically, the S&P 500 has returned about 10% annually. If your mortgage is sitting at 4%, that's a potential 6% gain you're leaving on the table.

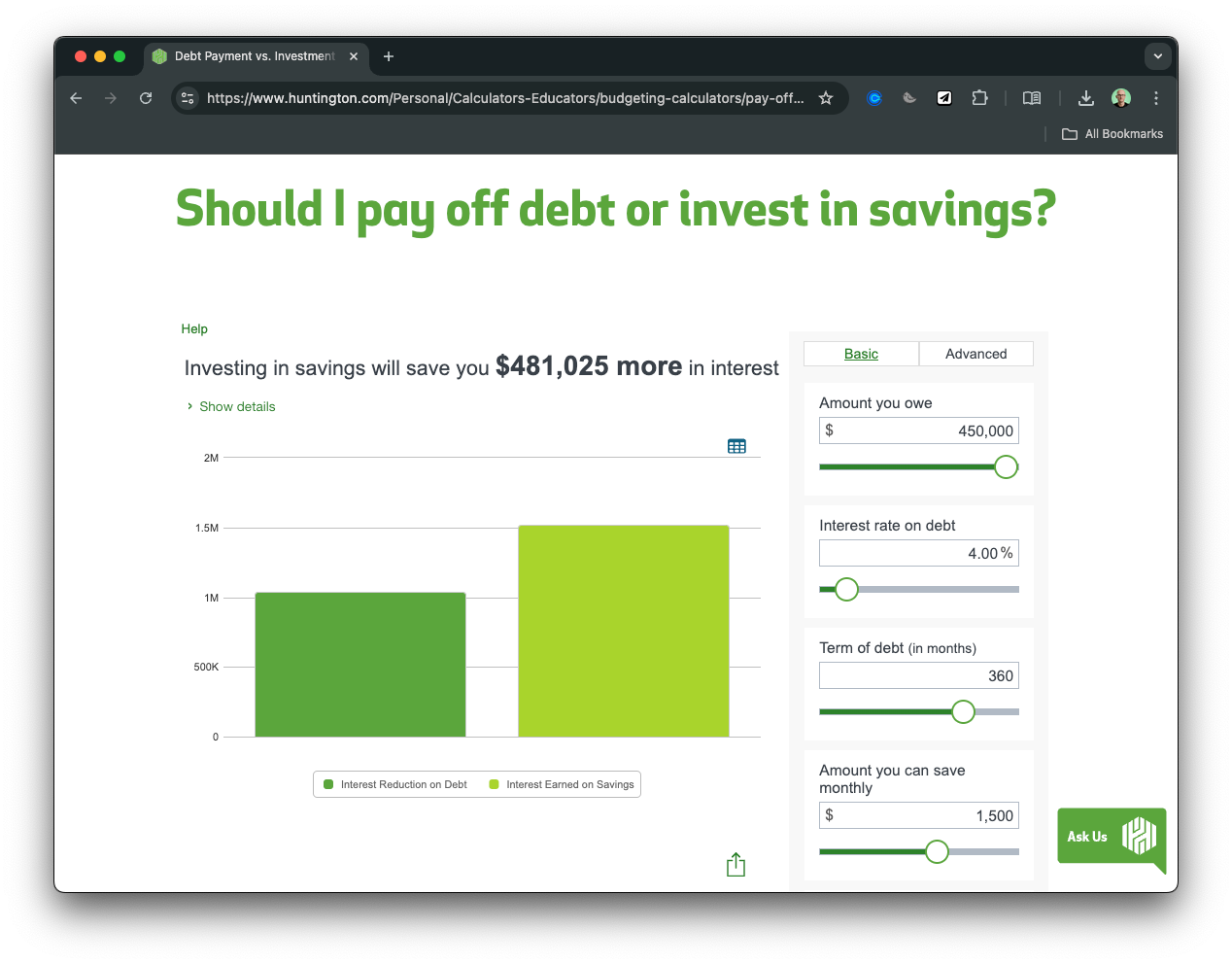

Let's look at a real-world example:

Imagine you have a $450,000 mortgage at 4% interest with a 30-year term. You have an extra $1,500 per month to either invest or put towards your mortgage.

If you invest that money in an S&P 500 index fund (assuming the historical 10% average return), after 30 years you'd end up $481,025 better off compared to using that money to pay down your mortgage early.

But remember, we're playing the long game here. Short-term market volatility is a given, but over time, the math often favors investing.

2. Tax Deductions

I know, I know. The 2017 tax changes made this less impactful. But hear me out.

For some of us, mortgage interest is still deductible. This effectively lowers your interest rate. A 4% mortgage might only cost you 3% after tax savings.

It's not game-changing, but every bit counts when we're building wealth.

3. Inflation Hedge

Let's channel some Morgan Housel wisdom:

"Every bit of savings is a hedge against life's inevitable ability to surprise the hell out of you."

A fixed-rate mortgage? That's a beautiful hedge.

As inflation rises, your payments stay the same. In real terms, the payment is getting cheaper over time.

It's your weapon against the eroding power of inflation.

Reasons to Pay Off Your Mortgage Early

1. Guaranteed Return

Want a risk-free investment? Look no further than your mortgage.

Every extra payment gives you a guaranteed return equal to your interest rate. In a world of market uncertainty, that's golden.

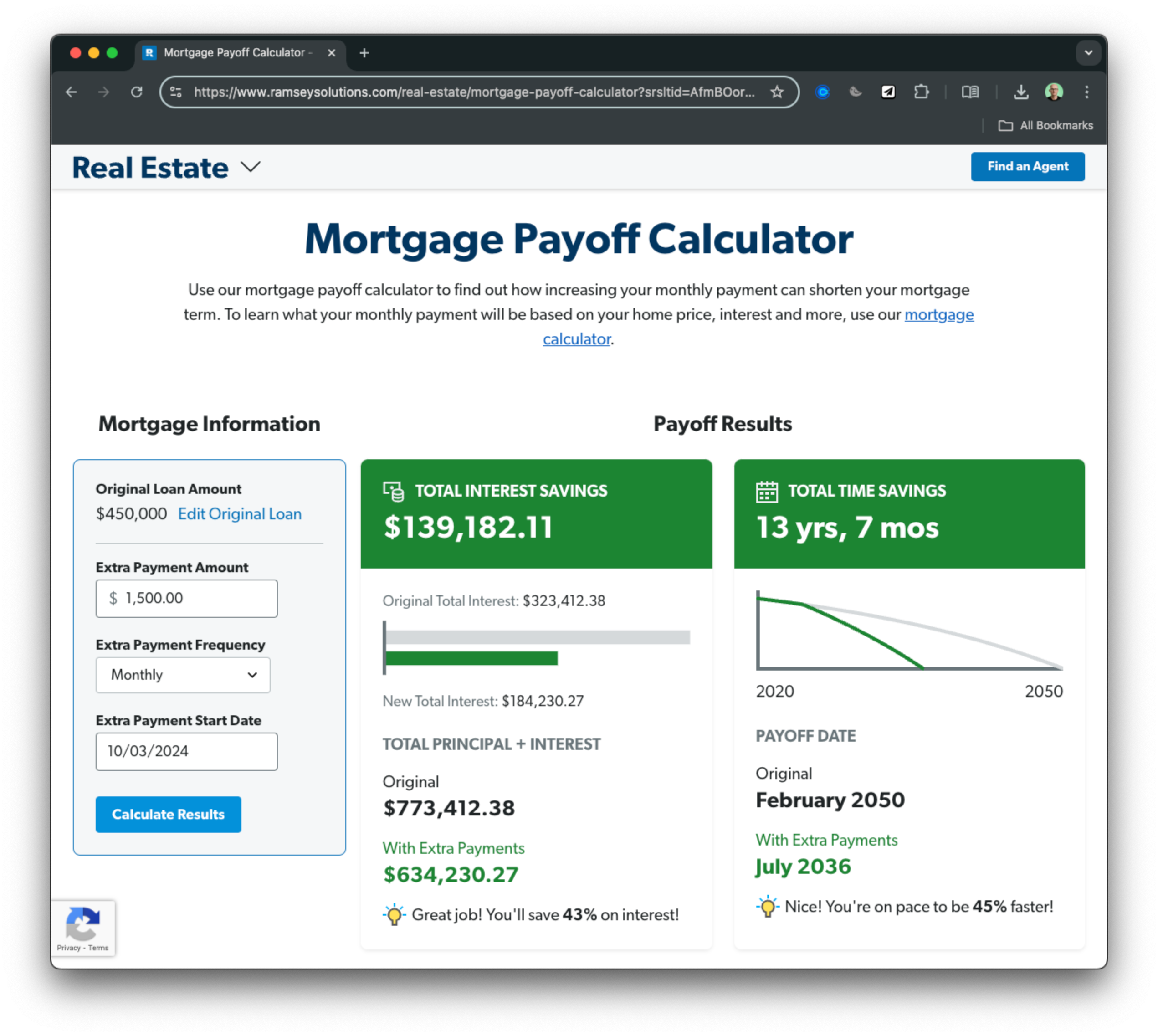

Let's look at another real-world example:

Say you took out a 30-year mortgage at 4% on March 31, 2020. Now, you're ready to start making extra payments of $1,500 per month. Here's what happens:

You'll save $139,182 in interest payments (that's 43% of your expected interest payments)

You'll pay off your mortgage over 13 years faster (45% quicker than the original term)

Once it's paid off, you'll have both your regular mortgage payment and that extra $1,500 to invest each month

Think of it as the world's safest bond, paying whatever your mortgage rate is. Not too bad, right?

2. Improved Cash Flow

Picture this: No mortgage payment. At all.

That's a chunk of change freed up every month. You could supercharge your investments, start that side hustle you've been dreaming about, or simply have more flexibility in your lifestyle and career choices.

As the saying goes, cash flow is king.

And no mortgage payments? That's like unlocking god-mode for your monthly budget.

3. Peace of Mind

Never underestimate the psychological benefit of being debt-free.

Peace of mind produces more returns than any amount of money ever will.

A paid-off home is your financial fortress.

It's security.

It's freedom.

It's sleeping well at night

Hybrid Strategy: The Best of Both Worlds

Can't decide between investing and paying off your mortgage?

You don't have to choose just one. Consider a hybrid approach that combines both strategies.

The 50/50 Split: Allocate half of your extra funds to additional mortgage payments and half to investments.

This strategy allows you to balance the benefits of both approaches, potentially giving you the best of both worlds. It offers flexibility and can be adjusted based on your changing financial situation or goals over time.

Making Your Decision

Here's the framework to guide your choice:

Compare your mortgage rate vs. potential investment returns

Weigh peace of mind vs. potential gains

What aligns with your personal goals?

Use these calculators to see how different strategies could play out for your specific situation.

Remember, this isn't just about math. It's about you and your financial journey. Whether you choose to invest, pay down your mortgage, or do a bit of both, the key is to start and stay consistent.

Thanks for reading. We'll see you next week.

Whenever you're ready, there are 2 other ways we can help you:

Opulus Method Digital Course: Join 350+ students inside the Opulus Method. In just 90 minutes, learn a proven system to secure your financial freedom without sacrificing your lifestyle.

Join Opulus as a Client: We'll build your personalized strategy to reduce taxes, boost your income, and grow your wealth. Live life on your terms—we'll execute the financial strategy to get you there.

Opulus, LLC (“Opulus”) is a registered investment advisor in Pennsylvania and other jurisdictions where exempted. Registration as an investment advisor does not imply any specific level of skill or training.

The content of this newsletter is for informational purposes only and does not constitute financial, tax, legal, or accounting advice. It is not an offer or solicitation to buy or sell any securities or investments, nor does it endorse any specific company, security, or investment strategy. Readers should not rely on this content as the sole basis for any investment or financial decisions.

Past performance is not indicative of future results. Investing involves risks, including the potential loss of principal. There is no guarantee that any investment strategies discussed will result in profits or avoid losses.

All information is provided "as-is" without any warranties, express or implied. Opulus does not warrant the accuracy, completeness, or reliability of the information presented. Opinions expressed are those of the authors, Ryan Greiser and Francis Walsh, and are subject to change without notice.

Opulus is not responsible for any errors or omissions, nor for any direct, indirect, or consequential damages resulting from the use or reliance on this information. Use of the content is at your own risk. This content is not intended as an offer or solicitation in any jurisdiction where such an offer or solicitation would be illegal.